Here are three economic risks.

#1: A crashing stock market.

#2: Ultra low interest rates.

#3: High inflation.

These three economic events can rob the purchasing power of your wealth.

Now we may have all three conditions… at once!

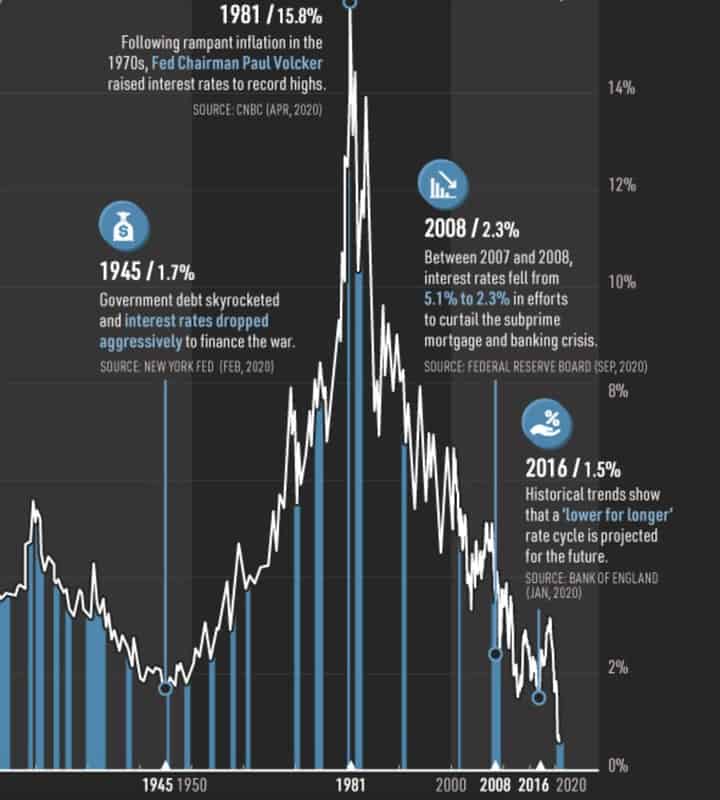

The ultra low interest has been with us for some time. We can see this in a chart at advisor.visualcapitalist.com/us-interest-rates

As inflation rips upwards, interest rates should rise, but as the chart above shows the government can keep rates lower than they should be.

Watch the stock market closely now. We can see how the danger is brewing everywhere.

A Wall Street Journal article yesterday entitled “Inflation Poses Risks of Faster, Less Predictable Fed Rate Increases” warned “Promises or clues about rate plans are growing harder to deliver”

A New York Times article “Wall Street’s losing streak stretched into a fourth week, and the S&P 500 has fallen 10 percent since early January”. reinforced the risk.

A drop of this scale is known as a correction — and is seen as marker of a shift in sentiment as the market adjusts to a new outlook on the economy and corporate profits.

Another Wall Street Journal article, “Tech Rout Fueled by Bond-Market Turn” helps explain why: Rising yields, particularly on inflation-protected Treasurys, are often viewed as close indicators of borrowing costs for businesses and consumers

Shifts within the bond market are removing a key pillar of support for Wall Street’s more speculative bets, dragging down major stock indexes as investors flee everything from tech stocks to cryptocurrencies.

Spooked in large part by rising bond yields, investors continued to dump stocks last week, extending early-year losses that have taken many off guard with their speed and severity. Once again, tech shares were at the forefront. Selling also broadened to include sectors such as banking and energy, sending the S&P 500 to its worst stretch of declines since the onset of the Covid-19 pandemic.

We need a new wealth protection plan.

We are living in times like we have never seen. There’s huge differences and change in the economy so we need to rearrange how we think and act.

Embrace risk! Everything is risky now. Live with this fact and rewire your work, your investing and your thoughts. Planned danger is as safe as we can have.

Let me share how I’m doing this.

My approach might work for you. It might not. After all a 75-year-old must plan differently than someone who is 20, 30, 40, 50 or more.

But as we share, I’ll give you the tools to adapt this thinking to your own set of needs and desires.

My plan might be good one. Or it might not, because what we face is a known unknown. We need to think of our plans as short time starting points, that we monitor and adjust as we move ahead.

We start with knowing that we are in the unknown. Previously we might have been fooled into thinking that we knew what’s ahead. The 50 years of stability we enjoyed obscured the longer trends.

Now we know better. We are acutely aware that we are guessing more than usual about “what’s next”.

Locking our money in a safe is not safe, because safe is unsafe in our current turbulent world. Risk is our friend and we have to learn how to protect with risk.

The first and foremost step in my plan is to continue to be of service in creating wealth. In other words at the age of 75 I am still working and that’s OK. I love what I do and in the “Live Anywhere, Earn Everywhere” scheme of things, I can be at work wherever I choose to be.

After all 65 was created as a retirement age when the average lifespan was still in the 50s.

My own personal skills are where I am putting my greatest effort, because our ability to serve and be of value is the ultimate asset. All the other promises that our human hierarchy offers can fail, but having something to offer in the marketplace of mankind will always be an inflation-proof asset.

Next, I focus on investing to protect the money I have and any extra monies I save and to make these monies grow.

Second, I track and for equities invest only Index ETFs in good value stock markets.

I recognize that I no longer have decades to let my portfolio recover if we see a major long-term market correction.

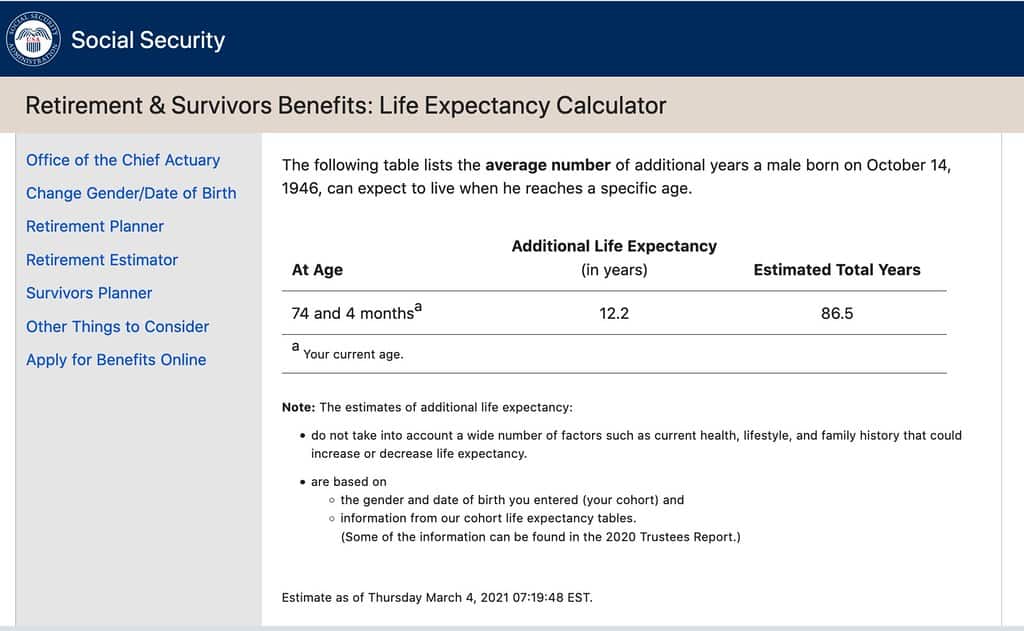

I make sure I know how long will I need this wealth I am trying to protect?

I can use a system offered by the US Social Security Office. It says I have 12.2 years to go.

I like the “How Long Will I Live” system created by some professors better. (This is the first tool to use in your wealth protection plan).

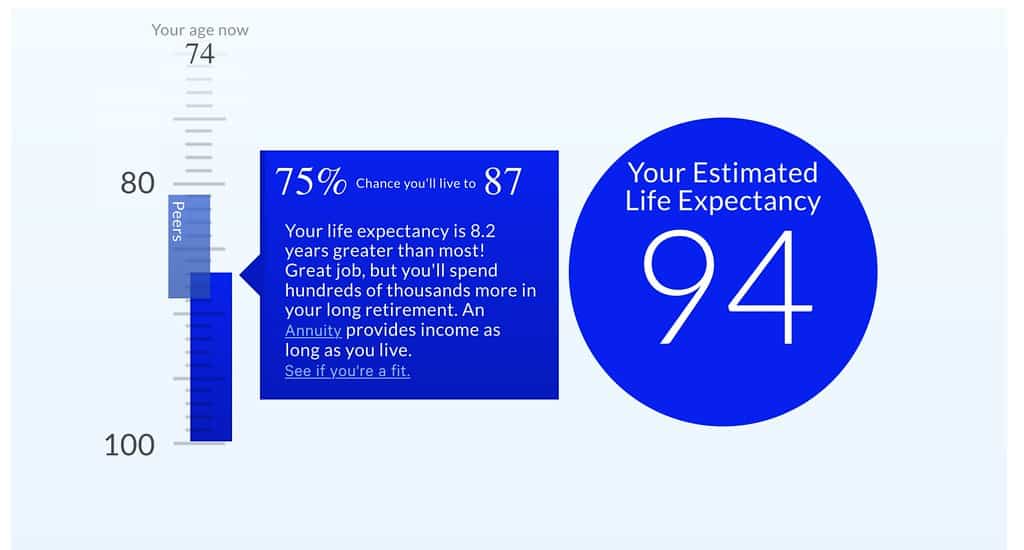

This system asks questions.

The “How Long Will I Live” system gives me an extra eight years. I’ll take that!

My mom made it to 96 (though dad did not make it to 60) and I believe a Welsh forefather reached 106. So I can let hope spring eternal and plan for at least 20 years.

Next I can go to (your second plan tool) another US government system, www.investor.gov/financial-tools-calculators/calculators/compound-interest-calculator and do some compounding math.

My research found that the average long-term return for a global growth equity index strategy was 8.36%.

So I’ll calculate, how much wealth these strategies will create in 20 years.

If the return I get is 8.36% I’ll have $498,172.70 in 20 years for each $100,000 invested.

Still I have no idea what will really happen, but I now have a time parameter and some numbers based on earning (8.36%) over the 20 years.

The chances of just getting positive results in a straight upwards motion are highly unlikely. In tho 20 years I am planning for (or however many years you have), we’ll likely see some volatility.

The question is how long do we need to hold an investment to get the best return?

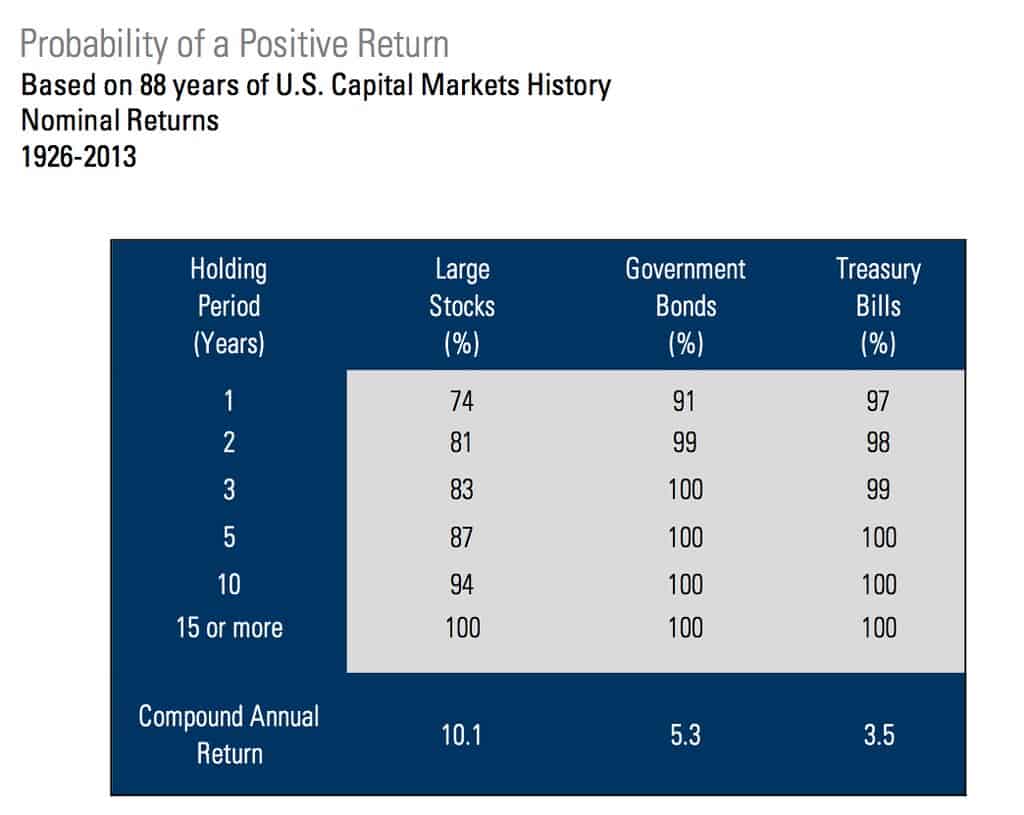

Here, we can turn to an 88 year Keppler Asset Management study on the probability of a positive and top return. (These numbers are the third tool).

The study shows that a diversified portfolio invested in US markets had a 74% chance of at least breaking (above) even and after 15 years, 100% chance that there will not be a loss.

After a year the odds are 63% that I’ll have the highest return on that portfolio and after 20 years I can be pretty sure that I’ll have the highest return, if I leave the portfolio alone.

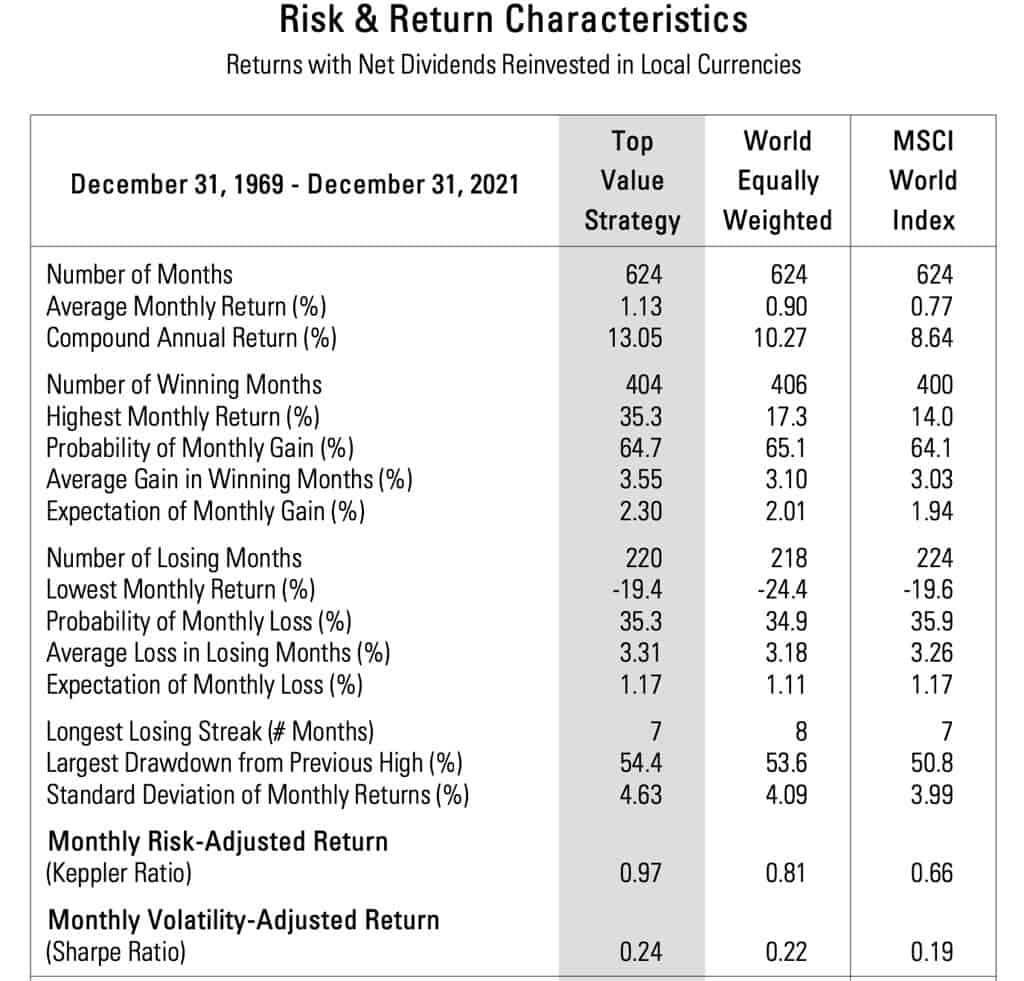

This gives us some odds to work with so I can now look at the risks of a draw down. The stats below (the fourth tool) show that longest losing streak (if we have the Top Value Portfolio) might be seven months and the largest draw down from the previous high is 54%. What we do not see in this information is how long the draw down might be and how soon the recovery.

So far my planning has looked at all the ups. I also have to consider the downs.

History suggests that if I invest in good value stock markets, given the passage of time, an inner calm, ample diversification and a minimization of transactions and fees, every $100,000 I invest with grow to somewhere around $498,172.

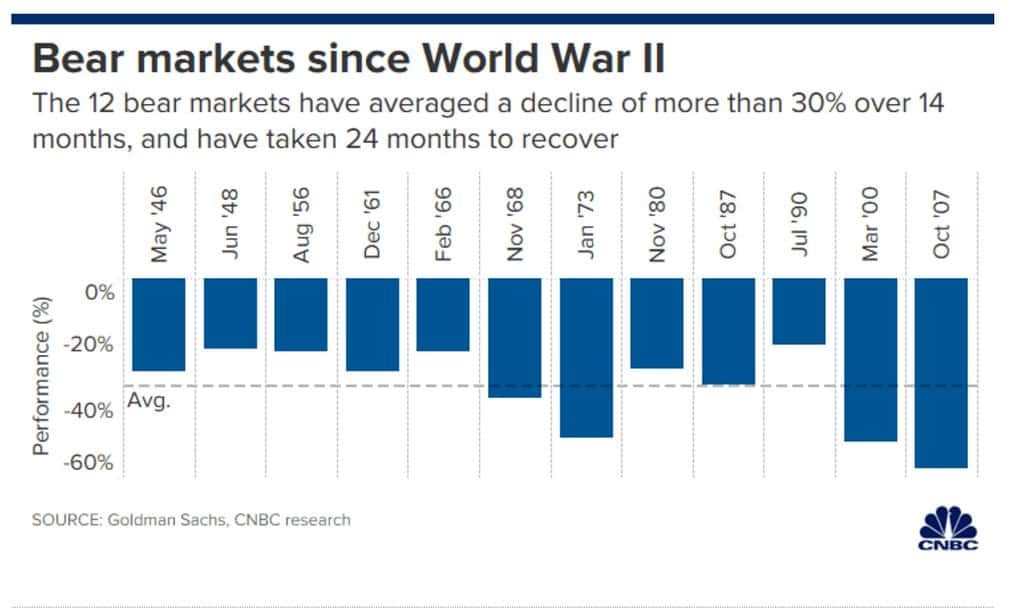

According to CNCB article “Here’s how long stock market corrections last and how bad they can get ” (1) which is the fifth tool I use, there have been 26 market corrections (defined as a 10% decline in one of the major U.S. stock indexes) since World War II with an average decline of 13.7%. Recoveries have taken four months on average, if the correction did not fall into bear territory (defined as a 10% decline in one of the major U.S. stock indexes).

Bear markets are the worst glitch

The CNCB article states that there have been 12 bear markets since World War II with an average decline of 32.5% as measured on a close-to-close basis.

These bear markets have lasted 14.5 months on average and have taken two years to recover on average.

During the October 2007 to March 2009 bear market, there was a 57% drop and the recovery took four years.

This downside information provides me with two data points.

The first point, the four months average recovery for corrections in the market. To cover this, I’ll make sure that I always maintain four months’ worth of immediate liquidity so I never have to liquidate holdings when markets are down during market corrections.

The second data point is the depth of loss and time for bear markets. I want tactics that allow me to maintain my portfolio for two years without requiring any liquidation.

In my case, I have created a balanced portfolio that includes income-producing real estate that generates enough cash flow so I don’t have to sell equities during bear markets . Assuming my plan holds together I can leave my equity portfolio undisturbed.

One other way I can reduce the risk of a forced sell-off is to increase the dividend income-producing element in the equities I hold. We’ll look at this tactic in an upcoming message.

That’s the basics of my plan I use. Hopefully it works. If so, I might sleep better at night (though there are other health and well-being plans for that we’ll review another time), never have to worry about day-to-day costs of living, and 20 years from today there will be something nice for the children and grandkids.

If my plan does not, ideally it’s because the time element was wrong. “Hey here I am, 94, thriving and active. Kids, you get me, not cash, for now”. They’ll be happy.

Yet I keep in mind that there are still risks of pandemics, civil disturbances, weather disasters, perhaps even a war or even something worse. I hope not, but that’s why my plan is a starting point, not an inflexible map.

We have all lived most of our lives in an era of relative stability. To keep society together and moving forward, many promises have been and are being made (pensions, Social Security, stable currency, insurance, health care, physical security, economic stimulation). Not all of these guarantees, maybe none of them, can be kept.

There are plenty of problems for humanity to solve. For example, 75 years after WWII, Western society is still at odds with Russia and China. Good grief. How can it be we have not settled this.

Yet here, we are 75 years later, more people, more material wealth with some amazing day-to-day stuff we could barely dream of in science fiction just a few decades ago.

My starting point is based on an optimism that mankind will evolve along lines based on humanity, compassion, friendliness, and recognition that cooperation blended with friendly competition might be the most productive, successful model.

Yet the plan is day to day short term in the sense that history suggests we’ll see obstacles and roadblocks that require adjustment.

I’m ready. I have a plan, flawed in many ways, but workable because it is meant to evolve and I’m ready to adapt because I recognize that risk is our friend and I have to accept more risk than before to be safe.

I hope the thoughts and the tools here can help you prepare a well protection plan that suits you.

Gary

(1) www.cnbc.com/2020/02/27/heres-how-long-stock-market-corrections-last-and-how-bad-they-can-get.html

Gary is an entrepreneur, author, and investment publisher who began writing about multi-currency portfolios five decades ago when many thought he was crazy.

Gary is an entrepreneur, author, and investment publisher who began writing about multi-currency portfolios five decades ago when many thought he was crazy.

Jackie, so nice to see you on here again….I hope you’re thriving still and I look forward to more content as well as re-engaging in so much that I’ve yet to explore and put to use. In our environment of everybody being an expert, all of a sudden, the volume of noise is and shiny objects is overwhelming…..I have a curiosity…many investors who have apparently met with some success seem to be nostalgic for the policies of our former leader in chief…albeit the discord engendered notwithstanding…i wonder if you have someone who could come on and offer a context to illuminate if in fact things were better business wise, how they were…and how to reconcile that with the grift and graft and fascist, authoritarian posturing with attendant loss of personal freedoms and suppression of rights that so egregiously mitigated a cooperative discourse between such polarized elements in our culture…If in fact business was greater, at what cost? Anyway….just a thought….I want to have a better understanding of the nature of the two beasts as I go forward….

HI Anthony, Business was definitely different 10,15,20 or 30 years ago. There were fewer rules and regulations which tend to suffocate a business. But a smart, well-trained creative investor, knows how to ZIG when everyone else is ZAGGING.

Anthony, thanks for this is an interesting question, but to try and put perspective on whether the left or right in politics is better for business throws us into the exact quagmire that politicians desire.

The correct answer is that the political system, especially at this stage of America’s economic cycle, has little to do with the economy and any government is dangerous.

My publications for the past 50 years have worked on the principle that regardless of the government’s position (left or right) they should be avoided as much as possible.

The first book I wrote in the 1970s was entitled “Passport to International Profit” and looked at how governments take advantage of what I call the “Soil Defense Syndrome”.

One chapter in that book described the “Concept Conversion Trick” and how it creates the soil defense syndrome.

The book said: “The Concept Conversion Trick begins when people agree on a good concept for working and living together. The people go to work and if the concept is good they will create a paradise. The government gives them a flag and a song. Then the government pulls the trick. The government convinces the people that the flag and song are important. Then while the people are busy watching the flag and singing the song, the government replaces the original concept with a set of ever increasing written rules and regulations administered by bureaucrats and backed up by a police force.

“This trick trades people’s individual freedoms for a shiver up the spine when the song is played and the piece of cloth is waved.

“The Concept Conversion Trick turns spirit into matter.

“Like trading love for a beautiful plastic doll. When the trick has been pulled and the dust settles, the people realize too late what has happened. Anyone who steps out of line is called unpatriotic or even criminal. He is swatted down by the bureaucracy or police force, crushed with overwhelming power or made an example of so others will tow the mark ‘for the good of society’. All this is done in the name of public interest.”

If this writing sounds prophetic having been written over 50 years ago, it was not.

Any simple review of any previous great society shows this trick and evolution. Like the Roman Empire , things may get better for a while, then worse and then better again. In the long term, as societies age, they lose their original vibrancy and life. The left and the right fuss and argue but all take, take, take from our wealth and freedom.

Should we be surprised? Does not every single thing in this universal existence develop in the same way, vibrant and flexible while young and growing thicker and more brittle with age?

The world is as we should expect.

If there is a problem it’s not the economy, the politics or the changes around the world. The difficulty lies in our thoughts and beliefs when they are not in tune with reality.

Maybe the pandemic has moved things along a little faster and sent the current down cycle a little deeper than than we would expect, but the downturn should be expected. We could be surprised by the severity and speed of decline caused by COVID-19, but our 2017 report “Live Anywhere – Earn Everywhere” looked at the risk of how America would respond to a viral infection. History provides us clues to the fact that current events are normal when looked at in the long term norm.

Long term thinking is what we need. When we cannot understand what’s happening right in front of us, we have to rise above the day to day obstacles and gain a broader historical perspective.

Nothing that’s happening now is new in the bigger picture.

Nature works in bell shaped curves and human beings (surprise-surprise) are part of nature. Our actions, our societies, successes and failures are controlled by this reality too.

So, let’s get on a positive note. Material affluence in human society has been rising for millennia. However this increase comes in waves with up and down cycles.

Over the past decades, mankind has moved thru seven industrial eras since the 1750s.

These eras are best described by Joseph Schumpeter, on how innovation creates industrial revolutions altering the way we live, work, earn and keep money. He described five great economic eras that began in the late 1700s:

Era #1: 1785-1845-fueled by water power-60 years. Textiles and iron works were the backbone of growth industries.

Era #2: 1845-1900-fueled by steam-55 years. Railways and steel provided the main growth in this era.

Era #3: 1900-1950-fueled by the internal engine-50 years. Electricity and chemicals provided the major growth.

Era #4: 1950-1990-fueled by electronics-40 years. Petrochemicals and aviation were the innovations which became mainstream in this period.

Era #5: 1990-current-fueled by digital networks- 30 years+ ? Software and new media create the growth elements in this era.

Each era greatly empowered massive new numbers of individuals, an empowerment that led to entire new social and economic classes. The working middle-class was born. This empowerment allowed the working class to rise from feudal subservient positions to positions of economic and hence political influence. Even in terrible global recession of the 1930s, people were far better off materially than a century before.

Much of the world’s population became much richer in each era, but these advances were accompanied by turmoil caused by periods when the old order had not let go and the new order had not taken hold. Many forces came into play and there were struggles for dominance to establish order.

We are in one of these turbulent periods now where social networking has become a dominant force, but has not gained full dominance.

We can see these forces if we examine the last three reserve currency nations that rose to become the leading global power and then saw their dominance fall.

From the 1500s to the mid 1750s, the Netherlands was the leading power. In the mid 1700s the British Empire took the lead and was not passed as the supreme power until around 1900 when the USA surged ahead until about 1950.

In the Dutch era, Amsterdam was the world’s financial center and the Dutch guilder became the world’s reserve currency. London and the British pound took over these roles as Britain rose. Then the US dollar became the world’s reserve currency in 1944 and was as good as gold (or silver) until Richard Nixon reneged on the American currency promise.

Each nation rose and has fallen because nature runs in a bell shaped curve and within every success lies the seeds of decline.

Growing wealth and power have generally come from a (or many) new innovation that helps one or two countries become a leading power in the world. Then the hubris of success takes over, the power declines and some new technology creates a new leading power.

This change does not spell disaster. There can be decline, but affluence can remain. The Days of Dutch glory are long gone, but I have spent a lot of time in the Netherlands (I maintained an office and worked from there for years). I promise you, Holland is still a really great place to live.

The UK’s dominance has been in decline for over a century. I lived in England for more than a decade and am there often. English life can be absolutely superb!

The trick is to ignore as much as you can the hype from the politicians whether they are liberal or conservative. They all want your money!

Find and live in a pocket of affluence and do something that is of value to others and that makes you happy.

Terrific article with some very sage advice.